Xavier Pennington, Lead Columnist, Systems & Macro-Trends

June 17, 2026 · 19 min read

Why Community Solar Rates Fail to Save You Money

Community solar is sold on a simple arithmetic claim: subscribe to a share of a solar farm, receive credits on the utility bill, and pay less for electricity without installing panels on the roof. The advertised savings range is usually 10% to 20%.

That gap is not a marketing accident. It is the operating space in which many community solar offers live. The customer sees “solar credits” on one side of the bill and a separate subscription charge on the other. Between them sit rate design, administrative overhead, annual escalators, and net-metering rules that can convert a clean-energy discount into a marginal gain—or, in some cases, a net cost increase. The practical problem is not whether community solar can work. It can. The harder problem is how to check why community solar rates fail to save you money when the bill itself is not designed to make that answer visible.

The Anatomy of a Subscription: Why Fees Outpace Energy Credits

Community solar has an elegant physical structure and a messy financial one.

The physical structure is straightforward. A developer builds or operates a solar array. Households or businesses subscribe to a share of its output. The electricity enters the grid. The subscriber receives bill credits tied to the production of that share. No rooftop, no personal inverter, no permitting friction at the customer’s home.

The financial structure is where the machine becomes less benign. The subscriber usually does not receive electricity directly from the solar project. They receive a credit on the utility bill, then pay the community solar provider a separate subscription fee. Savings occur only if the credit is worth more than the fee.

That sentence is the entire system. Everything else is detail. But the detail is where the value leaks.

A typical community solar proposition has four moving parts:

1. The bill credit rate. This determines how much value the subscriber receives for each kilowatt-hour allocated from the solar project.

2. The subscription charge. This is the payment owed to the community solar company or project sponsor.

3. The contract escalator. This raises the subscription charge each year, commonly in the range of 1.5% to 3%.

4. The utility tariff architecture. This decides which parts of the electric bill the credit can offset and which charges remain untouched.

If the credit tracks the retail electricity rate and the subscription is priced at a stable discount, the model can produce savings. If the credit is discounted, the subscription rises automatically, or the bill contains fixed charges the credit cannot touch, the savings deteriorate.

The consumer-facing language does not usually clarify this. “Save up to 20%” compresses a dynamic calculation into a static promise. “No panels, no upfront cost” is true but incomplete. The absence of upfront cost does not mean the absence of embedded cost. It means the cost is routed through subscription pricing.

Community solar fails financially not because sunlight is expensive, but because the contract can absorb the value before the household ever sees it.

This is a structural issue, not an anecdotal one. Community solar developers face real costs: project development, financing, interconnection, subscriber acquisition, billing integration, customer service, and churn management. The problem is that the final subscriber often has no clean view of which cost is being recovered, at what margin, and under what escalation formula.

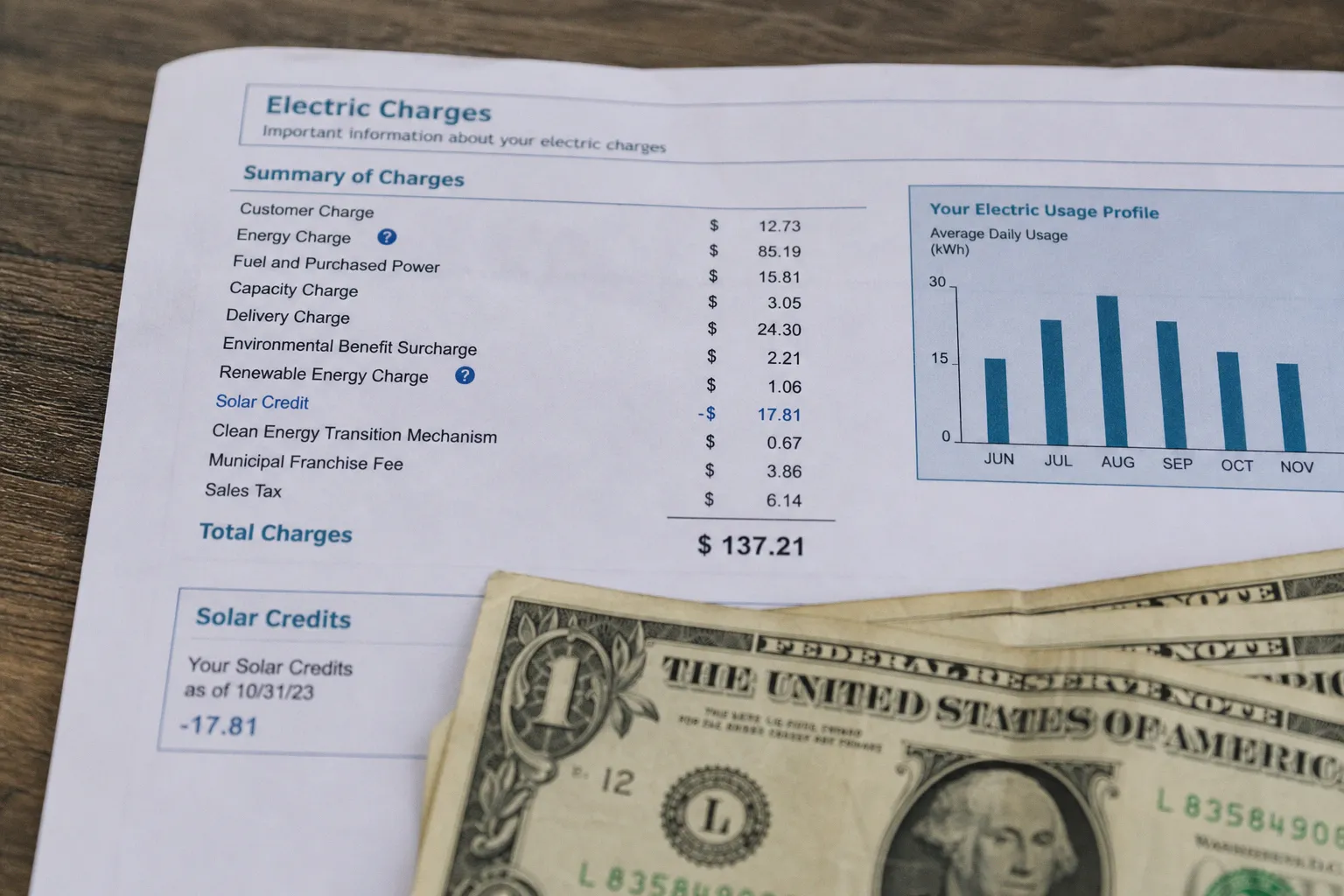

The utility bill compounds the opacity. Many billing statements do not clearly show how credits are calculated against the retail rate. Some list solar credits as a line item without showing the underlying kilowatt-hours, credit price, or offset category. The subscriber is left comparing two documents: the utility bill and the community solar invoice. That is not transparency. It is reconciliation labor outsourced to the customer.

Decoding the Bill Credit: Retail Rates vs. Avoided Cost Policies

The central variable in community solar economics is the bill credit rate. It sounds technical. It is decisive.

If the credit is valued at or near the retail electricity rate, the subscriber is credited as though the solar output offsets the electricity they would otherwise buy from the utility. If the credit is valued at an avoided cost rate, the utility effectively credits the subscriber closer to what it avoids paying for wholesale generation or other system costs. That rate can be materially lower.

The difference is not cosmetic. It changes the economic foundation of the subscription.

| Parameter | Retail-rate credit | Avoided-cost credit |

|---|---|---|

| Credit basis | Close to the customer’s retail electricity rate | Utility’s estimated avoided supply cost |

| Subscriber value | Higher, because credits offset more of the bill | Lower, because credits are discounted |

| Savings stability | More likely if subscription fees are controlled | Fragile unless the subscription price is also low |

| Customer visibility | Often still confusing, but easier to compare with normal rates | Harder to audit without tariff detail |

| Main risk | Fees and escalators consume the spread | Credit value is too weak from the start |

The policy choice determines who captures the value of distributed solar generation. Retail crediting gives more value to the customer. Avoided-cost crediting retains more value within the utility and system-cost framework. Regulators may defend avoided-cost methods on the grounds that grid maintenance, transmission, and fixed infrastructure costs still exist. That argument is not frivolous. But for the subscriber, the result is simple: the credit may not be rich enough to create meaningful savings after fees.

This is why the phrase “solar credit” is insufficient. A credit is not a savings. It is a number created by a tariff. The question is what the tariff allows that number to do.

A community solar subscriber should be able to answer three questions from the bill and contract:

- What is the credit rate per kilowatt-hour? If the bill shows dollars but not the energy quantity or rate, the subscriber cannot verify the calculation.

- Which utility charges can the credit offset? Some fixed charges, delivery charges, taxes, or program fees may remain even when credits appear generous.

- Does the credit rate move with retail electricity prices? If utility rates rise but the solar credit does not rise in parallel, the advertised hedge against energy inflation weakens.

This is where the comparison with rooftop solar becomes misleading. A rooftop owner may receive direct on-site consumption value, net-metering benefits where available, and tax incentives. A community solar subscriber receives a contractually mediated credit. The physics may be solar in both cases. The finance is not equivalent.

That distinction matters more after federal incentives expanded under recent climate legislation. The policy environment has become more favorable to solar deployment. But favorable deployment economics do not automatically translate into household savings. Incentives can lower project costs, strengthen developer margins, support low-income programs, or accelerate buildout. The allocation depends on contract design and regulation.

A decarbonized grid is a public objective. A lower household bill is a private outcome. They are related, but they are not the same thing.

The Escalator Trap: How Annual Fee Hikes Erode Long-Term Value

The escalator is one of the most underestimated clauses in energy subscription contracts. It is also one of the easiest to model.

Many community solar agreements include an annual increase in subscription fees. A 1.5% to 3% escalator can sound modest. It is framed as routine inflation protection for the provider. Over a long contract period, however, it changes the economics materially. The subscription price compounds. The bill credit may not.

The critical comparison is not escalator versus today’s inflation. It is escalator versus the growth rate of the credit value. If the subscription fee rises faster than the bill credit, the savings spread compresses. If the spread was thin at the start, it can disappear.

Consider a simplified structure. A subscriber receives $100 in solar credits in a given month and pays the provider $90. The gross saving is $10. That is a 10% discount on the credit value.

Now assume the subscription charge rises 3% annually while the credit value remains flat. The $90 fee becomes roughly $92.70 after one year, $95.48 after two, and $98.35 after three. The nominal saving has fallen from $10 to $1.65, before considering any fixed utility charges that credits cannot offset. If the credit drops because of tariff changes or production variation, the account can turn negative.

This is not an exotic failure mode. It is the predictable output of a contract in which costs compound and benefits do not.

The escalator becomes especially consequential in programs marketed as “no upfront cost.” Consumers correctly read that as lower entry friction. They often incorrectly read it as low long-term risk. In reality, the lack of upfront payment can make the back-end terms more important. The provider has to recover costs somewhere. A long-duration payment stream with an escalator is one mechanism.

A competent audit starts by separating first-year savings from lifetime contract value. First-year savings are the bright object. Lifetime value is the actual instrument panel.

The relevant questions are blunt:

1. Is the escalator applied to the subscription price, the total invoice, or another base amount? Ambiguity here is dangerous.

2. Is there a cap on annual increases? A stated range is not the same as a contractual ceiling.

3. Can the customer cancel without penalty if savings vanish? Exit terms define whether the household can respond to deteriorating economics.

4. Are savings guaranteed, or merely projected? Many standard contracts do not guarantee savings at all.

5. Does the provider disclose a long-term savings model under conservative utility-rate assumptions? A model that only works under aggressive rate inflation is not a savings plan. It is a bet.

The escalator is not always abusive. Projects need predictable revenue. Financing requires stability. But a fair escalator should be visible, bounded, and logically connected to the credit mechanism. If the customer cannot tell why the fee increases while the credit does not, the contract has transferred rate risk downward.

Hidden Overhead: The 30% Tax of Customer Acquisition Costs

Community solar has a scale problem that rooftop solar does not solve and utility-scale solar does not face in the same way. It must sell fractional participation in a shared asset to many dispersed customers, then manage those accounts for years.

That creates overhead. Customer acquisition and administration can account for 20% to 30% of total project costs. In energy infrastructure terms, that is not trivial. It is a shadow tariff embedded in the subscription price.

These costs include marketing, sales commissions, enrollment systems, billing coordination, call centers, credit checks, attrition management, and compliance. None of these produces electricity. All of them must be paid.

This is the structural friction in the model. Community solar attempts to democratize access to clean energy, especially for renters, apartment dwellers, and households with unsuitable roofs. That access layer is valuable. But access is not free. The model replaces rooftop installation friction with subscriber-management friction.

The economics become weaker when the program relies heavily on retail customer acquisition. Door-to-door sales, digital ads, referral bonuses, and third-party enrollment platforms raise the cost per subscriber. If churn is high, the project must keep spending to fill subscriptions. Those costs can then appear indirectly as higher subscription rates or weaker discounts.

This is one reason utility-administered or well-regulated programs can sometimes deliver cleaner economics than fragmented private offers. A utility already has customer relationships and billing infrastructure. A private developer may be better at project execution and market formation, but it pays more to find and retain each customer. Neither model is automatically superior. The cost stack matters.

The broader media environment tends to compress this issue into lifestyle advice. Energy literacy is treated as a consumer habit rather than a billing architecture problem. That is why adjacent public-information spaces—from local policy coverage to practical household explainers such as day-to-day news and life guidance—matter when they help readers connect daily costs to the systems behind them. But community solar cannot be evaluated through sentiment. It must be evaluated through arithmetic.

A clean-energy subscription is still a subscription. If acquisition cost, billing friction, and churn are buried in the rate, the customer pays for the machinery before paying for the electrons.

This matters politically as well. Community solar is often positioned as an equity instrument. It can serve households excluded from rooftop solar. It can expand participation in the energy transition. Yet if low- and moderate-income subscribers are placed into contracts with opaque pricing and weak savings guarantees, the equity claim becomes unstable.

A program that expands access but not value is not a complete solution. It is a distribution channel.

The ITC Gap: Why Community Subscribers Miss Out on Federal Incentives

The federal Investment Tax Credit has been one of the key financial supports for solar deployment in the United States. For rooftop owners, the logic is direct: the owner invests in a qualifying system and can benefit from the tax credit if they have sufficient tax liability and meet eligibility requirements.

Community solar breaks that direct link. The subscriber usually does not own the physical asset in the same way a homeowner owns rooftop panels. The project owner or developer may monetize available incentives, but the individual subscriber often does not receive the federal tax benefit directly.

That difference is critical when community solar is compared to rooftop solar. Both may reduce emissions. Both may support renewable generation. But they do not offer the same balance sheet outcome.

The rooftop customer faces upfront cost, property constraints, maintenance questions, and long payback periods. In exchange, they may capture more of the asset value, including tax incentives where applicable. The community solar subscriber avoids installation and ownership risk. In exchange, they generally accept a smaller, contract-mediated benefit.

This is not a defect by itself. It is a tradeoff. The problem emerges when marketing collapses the distinction and implies that subscribing to a solar farm is financially similar to owning a system. It is not.

A clear comparison looks like this:

| Feature | Rooftop solar owner | Community solar subscriber |

|---|---|---|

| Asset ownership | Owns or finances a specific system | Usually subscribes to a project share |

| Upfront cost | Often significant unless financed | Usually low or none |

| Federal tax credit access | Potentially direct, depending on eligibility | Often not directly available to subscriber |

| Bill savings mechanism | On-site generation and net metering or export credits | Utility bill credits plus separate subscription charge |

| Main financial risk | Payback period, financing terms, roof suitability, policy changes | Credit rate, fees, escalators, cancellation terms |

| Upside | Higher potential long-term value | Lower participation barrier |

The Inflation Reduction Act strengthened the solar incentive landscape and helped push new attention toward community solar. That macro trend is real. But the subscriber’s monthly savings depend on whether incentive value flows through the contract. If the developer captures the incentive and still prices the subscription aggressively, the customer may see little benefit.

This is a classic pass-through problem. Public policy lowers cost at one point in the chain. The intended beneficiary may be downstream. Whether value reaches that beneficiary depends on competition, regulation, transparency, and contract design.

In mature markets, pass-through can be disciplined by comparison shopping. In community solar, comparison is harder. Offers vary by state, utility territory, crediting policy, project vintage, and subscriber class. A customer may not have multiple clean options. Even when they do, bill formats make apples-to-apples comparison difficult.

The result is a market that can look competitive at the enrollment page and opaque at settlement.

Auditing the Agreement: How to Find the Value Leaks

The phrase “how to check why community solar rates fail to save you” sounds awkward because the market itself is awkward. The failure is not located in one number. It is distributed across the contract, the utility tariff, and the bill.

A serious audit reconstructs the transaction from first principles: what value came in, what charge went out, and what changed over time.

1. Build a two-bill view

Do not analyze the utility bill alone. Do not analyze the subscription invoice alone. The savings calculation requires both.

For each billing cycle, capture:

- the solar credit shown on the utility bill;

- the kilowatt-hours or allocation quantity, if disclosed;

- the community solar subscription charge;

- any participation, administrative, or billing fee;

- remaining fixed utility charges not offset by credits;

- the net total paid across both bills.

The key number is not the solar credit. The key number is total electric cost with the subscription compared with what the customer would have paid without it. If the utility bill drops by $40 but the solar provider charges $38, the saving is $2, not $40.

2. Identify the credit-rate formula

The contract or program disclosure should state how credits are valued. If the language refers to retail rate, avoided cost, value of solar, tariff credit, or utility-determined compensation, those words are not interchangeable.

The audit should determine:

- whether the credit rate changes with utility retail rates;

- whether it is fixed for a period;

- whether it varies by season or customer class;

- whether delivery charges are credited or only supply charges;

- whether unused credits roll over and under what conditions.

A subscriber does not need to become a tariff lawyer. But they do need to know whether the credit is tied to the rate they actually pay. If not, the advertised discount may be built on a weaker base than expected.

3. Compare the subscription charge to the credit, not to the old bill

Sales materials often frame savings as a discount on electricity spending. The more precise comparison is subscription charge divided by credit value.

If a provider charges 90% of the credit value, the nominal discount is 10%. If it charges 95%, the discount is 5%. If fees raise the effective charge above the credit, the customer loses money.

This ratio should be tracked over time. A single good month is not evidence of a good contract. Solar production varies seasonally. Credits may arrive irregularly. Billing cycles may not align. The only reliable view is multi-month.

4. Model the escalator against conservative utility-rate growth

A contract with a 3% annual escalator can still work if credit values rise faster. But that assumption should not be accepted without scrutiny.

A conservative model should test three cases:

| Scenario | Utility credit growth | Subscription escalator | Likely result |

|---|---|---|---|

| Favorable | Credit grows faster than fees | 1.5% or lower | Savings may widen |

| Neutral | Credit and fees grow similarly | 1.5%–3% | Savings may remain thin |

| Adverse | Credit flat or reduced | 3% | Savings compress or disappear |

The adverse case is not pessimism. It is risk analysis. Energy policy changes. Tariffs change. Production varies. Contracts should be judged by resilience, not best-case marketing.

5. Read the cancellation and transfer provisions

Exit rights are the pressure valve. If savings vanish and the customer cannot leave cleanly, the risk profile changes.

The agreement should be checked for:

- minimum subscription period;

- early termination fees;

- notice requirements;

- transfer obligations if the customer moves;

- credit check or replacement-subscriber rules;

- provider rights to modify terms.

A no-upfront-cost contract can still impose friction at exit. That friction has economic value. If the subscriber cannot leave when the deal stops working, the provider has captured optionality.

6. Separate environmental value from financial value

This is the step many analyses avoid because it makes the conclusion less tidy.

A community solar subscription can support renewable generation and still fail to save money. It can be environmentally defensible and financially mediocre. It can be a useful decarbonization instrument but a weak household discount product.

These categories should not be blended. Blending them creates moral cover for poor pricing and false certainty for consumers.

For households with strong climate preferences, a small cost premium may be acceptable. For households joining primarily to reduce bills, it is not. The contract should be evaluated according to the subscriber’s actual objective.

Why the Market Keeps Producing Confusion

Community solar sits at the intersection of three systems that do not naturally produce clarity: regulated utilities, private project finance, and consumer subscriptions.

Utilities operate through tariffs that most customers never read. Developers operate through project economics that require stable revenue. Consumers operate through monthly bills and simplified claims. The result is a translation problem with money attached.

The market’s confusion is not accidental in the sense of being engineered by one villain. It is structural. Each participant sees a different ledger.

The utility sees system cost, interconnection, billing integration, and regulatory compliance. The developer sees acquisition cost, financing cost, subscriber churn, and project margin. The regulator sees program targets, grid impacts, low-income access, and political feasibility. The subscriber sees a promise: lower bills through shared solar.

The promise is the narrowest part of the system. It is also the part most exposed to failure.

Transparency efforts have improved in some jurisdictions, and consumer advocates have pushed for clearer disclosures. But there is still no uniform national reporting standard that lets subscribers compare realized savings across programs, utilities, and states. Data remains fragmented. That fragmentation benefits sophisticated actors. It burdens households.

A more functional market would require three reforms.

First, bills should show the credit calculation plainly: energy quantity, credit rate, eligible charges offset, and remaining charges. A line item labeled “solar credit” is not enough.

Second, contracts should disclose guaranteed versus projected savings in a standardized format. If savings are not guaranteed, the document should say so in direct language.

Third, escalators and fees should be presented as lifetime cost variables, not footnotes. A subscription with a 3% escalator is a different product from one without it.

These are not radical interventions. They are basic market plumbing. Without them, community solar will continue to depend on trust where arithmetic is required.

The Hard Conclusion

Community solar is not a scam category. That would be too crude and analytically lazy. It solves a real access problem in the energy transition. Millions of households cannot install rooftop solar because they rent, live in multifamily buildings, have shaded roofs, lack capital, or do not control the property. Shared solar can widen participation.

But the financial promise is narrower than the marketing suggests. Savings are not created by the existence of a solar farm. They are created by the spread between bill credits and subscription charges, after fees, escalators, tariff limits, and administrative overhead. If that spread is thin, unstable, or undisclosed, the subscription is not a savings product. It is an energy contract with uncertain value.

The central test is therefore mechanical. Track total payments. Decode the credit rate. Model the escalator. Identify fees. Check exit rights. Refuse to treat projected savings as guaranteed savings.

The energy transition will require mass participation, but participation cannot depend on opaque arithmetic. Community solar will deserve more trust when its bills become legible enough for ordinary subscribers to verify the claim printed on the enrollment page: that the cleaner option is also the cheaper one.